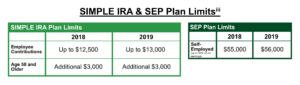

We have some exciting news to report for 2019 for those who are contributing to their retirement accounts! The IRS recently announced increases to the annual contribution limits to various types of retirement plans for 2019. With regard to IRA contributions (Traditional and Roth), this marks the first time since 2013 that there has been an increase to the annual limit. For 2019 those under age 50 may now contribute up to $6,000 to Roth or Traditional IRA accounts, up from $5,500. Individuals age 50 and older may continue to make a $1,000 catch-up contribution for the year, increasing their total contribution limit to $7,000 for 2019.

For those who qualify to contribute to Roth or Traditional IRA’s and have the means to do so, we encourage you to increase your contribution to the new maximum amount. Part of being a good steward of the resources that God has entrusted to us is preparing and planning ahead for future short and long-term needs (Proverbs 22:3). This is an opportunity to set aside a little bit more of your current earnings, to build additional wealth for retirement.

IRAs and Roth IRAs also offer the added benefit of tax deferral on growth that may occur in the account. In the case of the Roth IRA, while you do not receive an income tax deduction for your contributions, withdrawals have the potential to be tax-free once you have had the account for 5 or more years and are over age 59 ½. In this way there can be a tax benefit with regard to growth that may be attributed to the increased contributions to a Roth IRA.

Please contact The Life Financial Group to discuss whether increasing your Roth or IRA contributions for 2019 makes sense for you. Our Team is here to assist you in making the adjustments you need.

Article written by Jeremy Ehst

[1] Source: https://nb.fidelity.com/public/nb/default/resourceslibrary/articles/irslimits.

[2] In addition to the contribution limits discussed, your Modified Adjusted Gross Income can affect your ability to contribute to a Roth IRA, or make tax deductible Traditional IRA contributions. Please contact your Advisor to discuss how this affects your personal situation.

Securities and Advisory Services offered through GENEOS WEALTH MANAGEMENT, INC. Member FINRA and SIPC