Listen to President Tim Russell and Pastor Drew Gysi explore this topic here.

“But if anyone does not provide for his relatives, and especially for members of his household, he has denied the faith and is worse than an unbeliever.” (1 Tim. 5:8)

What a great passage of Scripture that speaks to the commitment that one ought to have for their family…especially those that are part of the immediate family and are on the elderly side! But today the cost of caring for the Elderly is, to say the least, off the charts! People are living longer and medical treatments are better…and also way more costly than they were even a handful of years ago! If it were up to the family alone to care for those that are aged in the family it would for many, if not most families, bankrupt them!

This is where, if you live in the United States, our Government stepped in many years ago and introduced a plan, and insurance that would allow medical care to take place not only for those that are elderly, but also for those with chronic disabilities that need extensive care and those with lower incomes.

The plans that are in place today are called Medicare and Medicaid. As we strive to understand Medicare & Medicaid, let’s jump in and take a look at these plans, along with their costs and benefits.

The History of Medicare

In July of 1965, President Lyndon B. Johnson signed a Medicare bill into law so that people 65 and older could get the healthcare coverage they needed from a national program. As of today there are over 64 million people who have coverage from the US Government sponsored healthcare called Medicare.

What is Medicare?

Medicare is a national United States health insurance program for people 65 and older. Medicare is also for people with certain disabilities or end-stage kidney failure. This program is divided into various parts, and it’s important to learn how these fit together.

For those that are under 65 and have a medical disability, and they are eligible for Social Security Disability Insurance (SSDI) benefits, they are also eligible for Medicare after a 24-month qualifying period. The first 24 months of disability benefit entitlement is the waiting period for Medicare coverage…and in that first 24 months, a person’s work healthcare coverage or similar will be priority coverage.

The Parts of Medicare

There are different parts of Medicare and they each serve a different function or part of your total health care coverage. Not everyone will be on all parts of Medicare. The costs will vary depending on the ‘part’ you are on.

Medicare Part A – “Hospital Insurance”

Part A is hospital insurance that assists you with the cost of inpatient care and skilled nursing facility stays. This is for everyone as long as you signup/apply for it as you are required to do so. Part “A” also helps with things like hospice and home health care. In general, you should think of the inpatient hospital benefit as Medicare coverage for room and board in the hospital.

Part “A” coverage covers the cost of your semi-private room. However, it does NOT cover all of the treatments that might occur in a hospital or clinical setting, such as outpatient surgeries. Those medical needs most likely will fall under Medicare Part B, which we will explain in a few minutes.

The cost of Part A for most people at age 65 is $0.

The reason why Part A is free is because during your working years you have paid taxes to pre-fund the premiums for your hospital benefits. You can also get Part A for $0 through a spouse or ex-spouse’s work history. Even if you don’t automatically qualify for premium-free coverage, most people age 65 can still get it – they would just pay a hefty premium for it.

Medicare Part B – “Outpatient Medical Coverage”

Part B is your outpatient medical coverage. Part B covers essentially all of your other medical services outside of your inpatient hospital care. Without Part B, you would be uninsured for doctor’s visits (and this would include any and most likely all doctors who treat you in the hospital). If you do not have Part B, you would also forfeit the Medicare coverage for lab work, preventive services, ambulance services and outpatient surgeries. This could add up with just one hospital visit!

One very important aspect of Part B coverage is that it does cover cancer therapy and kidney dialysis. This is HUGE today with the many forms of cancer that are challenging many people today. As you most likely know, cancer treatments are extremely expensive items that would cost a fortune without Part B and supplemental coverage.

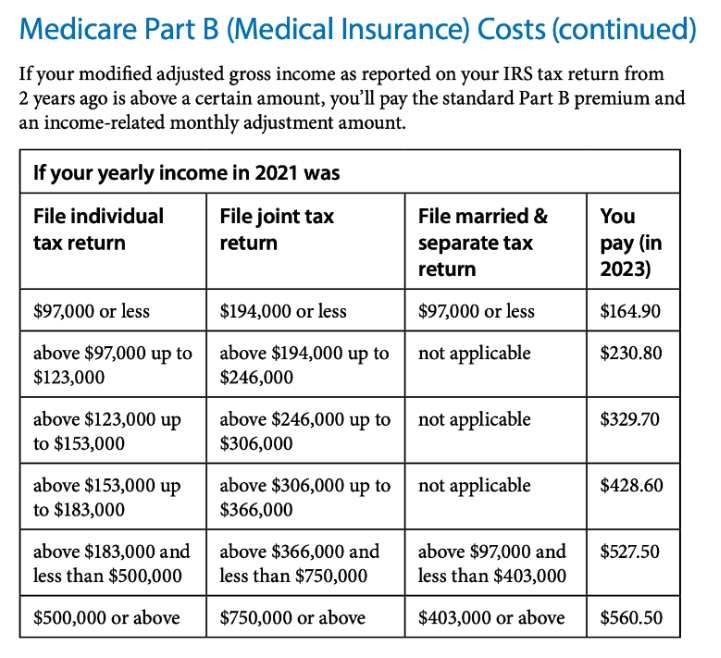

The cost of Part B is set by Social Security and one should expect it to change from year to year. Those that are in higher income brackets will pay more than those in lower incomes brackets. How this is done is through your modified adjusted gross income reported to the IRS. They take that number and they determine what your Part B premium will be. So, if you have a low income year, most likely in the following year two after this income is reported, your payment would be reduced. And conversely if you have a high income year, expect your next year of Part B payments to see an increase in relationship to what your increased income was for that two years later.

If you would have a substantial increase of income one year and not expect the same in the upcoming year or two, it would be prudent to tuck some money away knowing that this Part B premium increase is delayed! “Look ahead and see the evil”…(Prov. 27:12)…and that evil is a delayed Part B premium increase two years down the road!

One other key understanding of Part B coverage is that there is a 10% surcharge on medicare part B premiums for each year you go without signing up for medicare part B starting the month you are eligible for coverage. You will have to pay this penalty every time you pay your Medicare Part B premium indefinitely. This is a huge and ongoing penalty! It is important to make sure that you sign up for Part B, if interested, when you sign up for Part A.

Cost: It is approximately $164.90 premium per month w/ $226 Deductible (as of January 2023) if your AGI is individually less than $97k or jointly $194k

See more costs of Medicare here –> https://www.medicare.gov/basics/costs/medicare-costs

Medicare Part C – “Medicare Advantage Program”

Part C refers to the Medicare Advantage program, or private insurance. The cost of Advantage plans varies by carrier, county of residence, and plan selected, which are many.

To enroll in a Part C plan, you must first be enrolled in both Parts A and B. Even if you find a Part C plan with a very low premium, you will still pay for Part B. You must also live in the plan service area and apply during a valid election period.

Once you enroll, your Medicare coverage will come from the Advantage plan itself, not from the government.

The reason you don’t enroll in Part C at Social Security is that Part C is voluntary.

Many people prefer to get their Medicare coverage from Original Medicare and traditional Medigap plans. These people do not want a Part C Advantage plan, so they will simply not enroll in one.

Medicare Advantage (Part C) has more coverage for routine healthcare that you use every day. Medicare Advantage plans may include: Routine dental care including X-rays, exams, and dentures; Vision care including glasses and contacts (Anthem.com).

It is your choice whether you wish to opt for one as opposed to just staying with your original Medicare A & B. It is important to know that enrollment in Part C is only allowed (or open for enrollment) certain times of the year. So, if a change is desired, you will have to wait for the “open enrollment” time.

Cost: Varies depending on the plan and the features within that plan that are elected.

Medicare Part D. – “Prescription Drug Coverage”

This is the newest part of the US national health insurance program for people aged 65 & up. For more than half a century, there was no Medicare coverage for prescription medicines. In 2006, our federal government rolled out and elected Part D and tens of millions of Medicare beneficiaries signed up to get coverage for their outpatient drugs.

Part D covers many of the common retail prescription drugs that you pick up yourself at the pharmacy or order via mail order pharmacies available today. What you will need to do is choose a carrier and enroll in their drug plan, and that’s how you sign up for a Part D drug plan. Most states have about 30 drug plans to choose from. However, the best way to determine which one is the right fit for you is to work with a Medicare Enrollment Agent and have them run a Part D analysis using Medicare’s prescription drug finder tool.

Cost: As always, the monthly premium will vary depending on the plan that you choose.

It is also good to note that as per Part B, the ultimate cost for any of these plans (except for Part A) will vary depending on income from 2 years prior.

“Look ahead and see the evil”…tuck some $$ aside for it will be needed in the future if you are electing the “add-on” plans of Part B, C and D.

Click here to see Medicare Costs as of 2023

Medicare vs. Medicaid

A common question asked by many is how is Medicare different from Medicaid?

By definition, Medicare is a health insurance program for the elderly.

Medicaid, on the other hand, is financial and/or healthcare assistance for low-income individuals.

There are plenty of situations where some people 65 and older are able to qualify for both. When that happens, Medicare is primary insurance and Medicaid becomes the secondary insurance for the individual. The government has several Savings Programs which you can apply for through your state’s Medicaid office. These may help you to pay your Part B premiums as well as provide drug plan assistance. If you think you qualify, you would need to check with your state’s Medicaid office to see what their requirements are for enrollment. Since there are these two different coverages, Medicare and Medicaid, it would be good to take some time and briefly do a broad brush-stroke overview of what is and is not covered in the various plans.

What DOESN’T Medicare Cover?

- Long-term care

- Hearing aids (this may change late in 2023 and into 2024 with some of the “build back better” funding stepping in to cover these expenses)

- Routine dental care

- Routine vision care

- Medical care outside of the U.S. (problem for those travelers! Supplemental plan needed in this case!)

- Dentures

- Plastic and/or cosmetic surgery

- Massage therapy

What DOES Medicaid Cover?

- Long-term nursing home care

- Hearing aids

- Home Health

- Transportation to medical care

- Dental Care (Optional)

- Vision care (Optional)

- Hospice

- More…

Income & Asset Limits

It is important to note that in order to qualify for medicaid, you must meet certain income & asset limits. The best way for one to know if they are eligible is to consult a financial professional to get specific numbers for eligibility, and this will vary state to state. Click here to read more about Medicaid eligibility in Pennsylvania.

View by State – https://www.medicaidplanningassistance.org/state-specific-medicaid-eligibility/

Any money that the applicant receives counts as income. Wages, pension, social security, IRA withdrawals, and stock dividends. Any and all sources of income count as income! With a married couple, only the income of the applicant is counted towards the income eligibility. The community spouse may be entitled to a Monthly Maintenance Need Allowance (MMNA).

There are attorneys that specialize in Elder care law, and can help with Medicaid Crisis Planning. If you are concerned about your situation, consider having a conversation with an Elder Law Attorney and a Financial Professional.

Stewardship Application

This is timely information not just for the individual, but also for their loved ones. There may need to be some guidance needed as they go through this process of signing up, looking at the various plans and also weeding through the various costs that will have to be built into their budget.

As that happens, and if the finances are tight, it is always good to remember Philippians 4:19, “And my God will supply every need of yours according to his riches in glory in Christ Jesus.”

God is the great provider, not our own income, or even our government! God is the one that gives us what we need to sustain us…

- Psalm 55:22 – Cast your burden on the Lord, and he will sustain you; he will never permit the righteous to be moved (ESV).

- Psalm 73:26 – My flesh and my heart may fail, but God is the strength of my heart and my portion forever (ESV).

In those times where one will be needing, and depending on Medicare and Medicaid, it is so comforting to know that our God knows, sees, and is always providing for us in those difficult and/or elderly years.

Material presented is property of The Stewardology Podcast, a ministry of Life Financial Group and Life Institute. You may not copy, reproduce, modify, create derivative works, or exploit any content without the expressed written permission of The Stewardology Podcast. For more information, contact us at Contact@StewardologyPodcast.com or (800) 688-5800.

The topics discussed in this podcast are for general information only and are not intended to provide specific investment advice or recommendations. Investing and investment strategies involve risk including the potential loss of principal. Past performance is not a guarantee of future results.

Securities and advisory services offered through GWM, Inc Member FINRA/SIPC